Bitcoin Frees You From a Banking System That Is Totally Anachronistic

Bitcoin removes unnecessary middlemen.

Technological progress is leading to a digitalisation of the world in all areas. This digitalisation of the world is gradually leading to the elimination of all intermediaries in many areas. I am talking here about all the trusted third parties that are added to exchanges between people and who come to guarantee that the conditions of a exchange are respected.

Of course, middlemen do not work for free. The more middlemen you have in an exchange between two people, the higher the fees will be.

In the world of supply chain, this is called disintermediation. If I take the example of farmers, we are seeing more and more fruit and vegetable producers seeking to sell directly to their customers in order to prevent third parties from entering the distribution chain.

These third parties do not add value, but they are prohibitively expensive.

Thanks to digitalisation, producers are increasingly able to reach their customers directly. Customers also benefit from lower prices they. It’s a win-win situation.

At the level of the banking world, the problem of intermediaries is also omnipresent. I will go even further, since I sincerely believe that the current banking system is totally anachronistic.

I’ll give you a telling example.

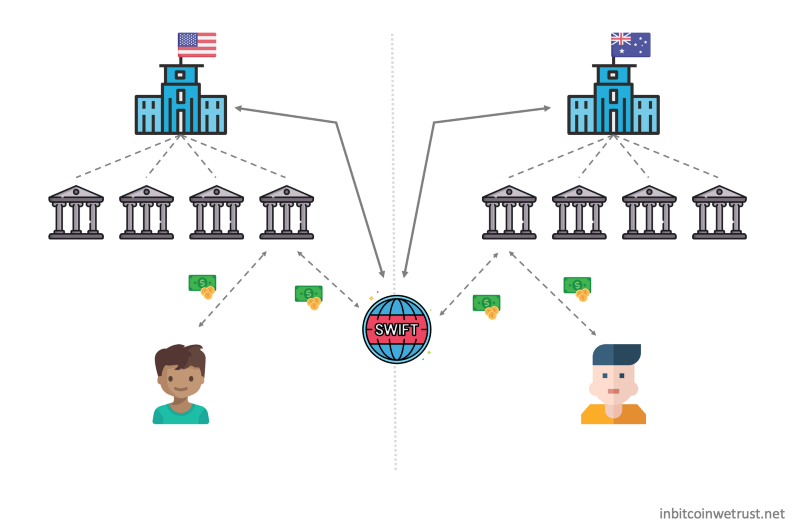

Let’s take the example of a cross-border transaction with the current banking system

Adam who lives in the United States has a bank account with $100,000 which he has managed to save by working hard. Nathan, one of his friends lives in Australia. For some private reason, Nathan needs $20,000 very quickly.

Nathan asked his friend Adam if he could lend him the money.

Adam has every right to lend Nathan $20,000, since he has $100,000 in his bank account. That money is his. He should be able to enjoy it as he wishes.

So Adam goes to his bank’s website, and tries to make a $20,000 transaction to Nathan’s Australian bank.

First failure.

His bank’s online site tells him that he cannot transfer such an amount over the Internet. Since it’s the weekend, Adam’s gonna have to wait until his bank branch opens. Nathan, that absolutely needs that $20,000, has to wait.

Adam goes to his bank branch, and explains that he wants to make a bank transaction to Australia for $20,000. Since it’s his money, Adam thinks it won’t be a problem.

Second mistake.

Adam’s U.S. bank is asking him to explain the $20,000 transfer. When you think about it, it’s pretty amazing. Adam worked hard to earn that money, and now he can’t enjoy it the way he wants to.

If Adam refuses to justify the reasons for the transfer, the bank may prohibit it, or even alert government authorities in the worst case scenario.

The risks of censorship with the current banking system are omnipresent.

Adam’s doing it. He explains that his friend Nathan needs the money for a specific reason. He has to reveal part of Nathan’s private life in order to be able to make his money transfer. There is a real problem of privacy.

Finally, Adam managed to initiate his transaction to Nathan’s bank.

So you think Adam did the hard part. Well no! The transaction hasn’t even come close to Nathan’s Australian bank yet. For an international transfer of this type, it will be necessary to use the SWIFT interbank payment network.

This implies delays of 2 to 5 days at best. In terms of transaction fees, Adam will soon be disappointed too.

The complete process of this simple $20,000 transaction between two friends is as follows:

As you can see, once the American bank has sent the bank transfer over the SWIFT network, the Australian bank will be contacted. Then the Australian bank can credit Nathan’s account.

Since private banks are attached to the central banks of their respective countries, the Fed and the Reserve Bank of Australia will be able to audit the transactions carried out by the banks attached to them.

Once Nathan’s account is credited, an acknowledgement of receipt goes the other way around. After a week, Adam was able to send the $20,000 to his friend Nathan in Australia.

The current banking system is anachronistic and flawed

Totally anachronistic, the current banking system highlights the limitations of such a centralized network. Transaction times are long and transaction fees high as each intermediary takes its fees.

Finally, the privacy of individuals is not respected.

In fact, you should have the right to use your money as you want without having to justify your reasons for spending $20,000. In the current banking system, you are deprived of this right.

Bitcoin provides an extremely simple and effective answer to this major problem of the banking system.

By creating Bitcoin, Satoshi Nakamoto wanted to address all the issues related to central banks in termes of monetary creation, but also in relation to private banks in which we cannot have total confidence:

“Banks must be trusted to hold our money and transfer it electronically, but they lend it out in waves of credit bubbles with barely a fraction in reserve. We have to trust them with our privacy, trust them not to let identity thieves drain our accounts. Their massive overhead costs make micropayments impossible.”

— Satoshi Nakamoto

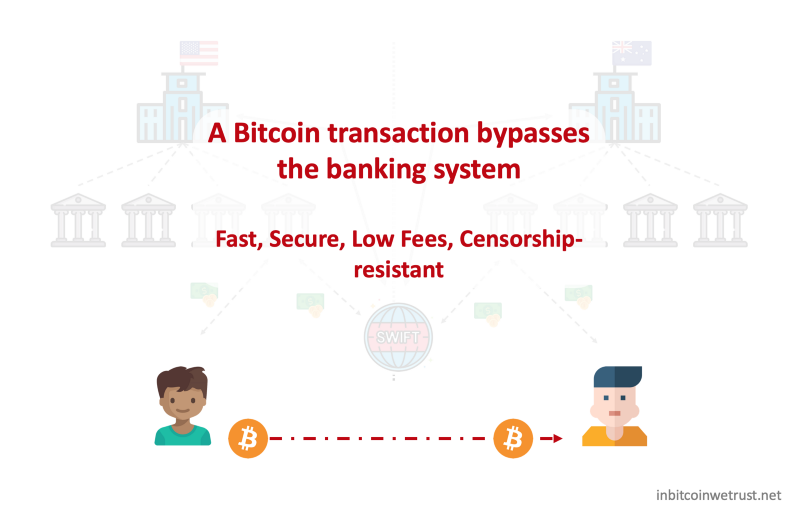

Now, let’s imagine the following with Bitcoin network.

Bitcoin is the best solution for cross-border transfers

Adam owns the equivalent of $20,000 in Bitcoin. So he decides to send this amount in Bitcoin from his wallet to Nathan’s wallet, who creates an address on the network for the occasion.

In approximately 10 minutes, Nathan’s address on the Bitcoin network is credited with the amount of Bitcoin transferred by Adam.

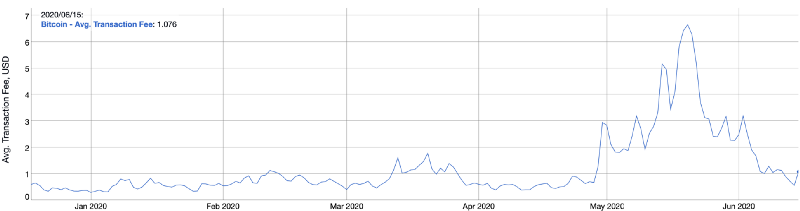

Even better, the transaction fees do not depend on the amount sent with Bitcoin. Whether you send $10, $20K, or $100 million, the transaction fees may be the same.

Most of the time, transaction fees on the Bitcoin network are between $0.50 and $1.00. Recently, they soared to $6.00 in May 2020, but this never lasts very long:

It is common for transactions of several tens of millions of dollars to be made over the Bitcoin network for transaction fees that remain below the one U.S. dollar.

Given the capabilities of the Bitcoin network, the banking system clearly can’t fight it.

Bitcoin frees you from the banking system by giving you the ability to bypass it completely:

The other obvious advantage of Bitcoin is that it has no leader.

In fact, no one’s going to ask you why you’re making a Bitcoin transaction with Nathan. No one will require justification or your transaction will be censored.

By making Bitcoin your own bank, you have at your disposal a fast, secure, low fees, and censorship-resistant tool.

Your Bitcoins can never be confiscated as long as you take care to keep their private keys safe.

With Bitcoin, you are in complete control. For this reason, Bitcoiners often say that Bitcoin gives power to the people.

Conclusion

Bitcoin works in a much simpler way because it does not require any middlemen that will charge you transaction fees. With its decentralized network, you have the near guarantee that the Bitcoin network is always running.

Bitcoin’s uptime of 99.98% since its inception is there to prove that.

Regardless of the time of day, and the day of the week, you will be able to use the Bitcoin network to make transactions. Bitcoin is therefore in line with history: that of the digitalization of the world and a regaining of control by the people.

As such, time is on Bitcoin’s side in the face of an outdated banking system that is flawed. Sooner or later, a majority of people will come to realize the superiority of Bitcoin.

Under these conditions, Bitcoin’s adoption can only increase sharply in the coming years.

1 Response

[…] Bitcoin Frees You From a Banking System That Is Totally Anachronistic […]